Insurance Requirements Traveling to Germany & Schengen Area

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

- Travel health insurance is not just a recommendation but a mandatory requirement for issuing a Schengen visa.

- The policy does not always have to be bought from a German or European insurer. Many embassies accept approved local insurers in the applicant’s country of residence, as long as the policy meets Schengen rules and claims are recoverable in a Schengen State.

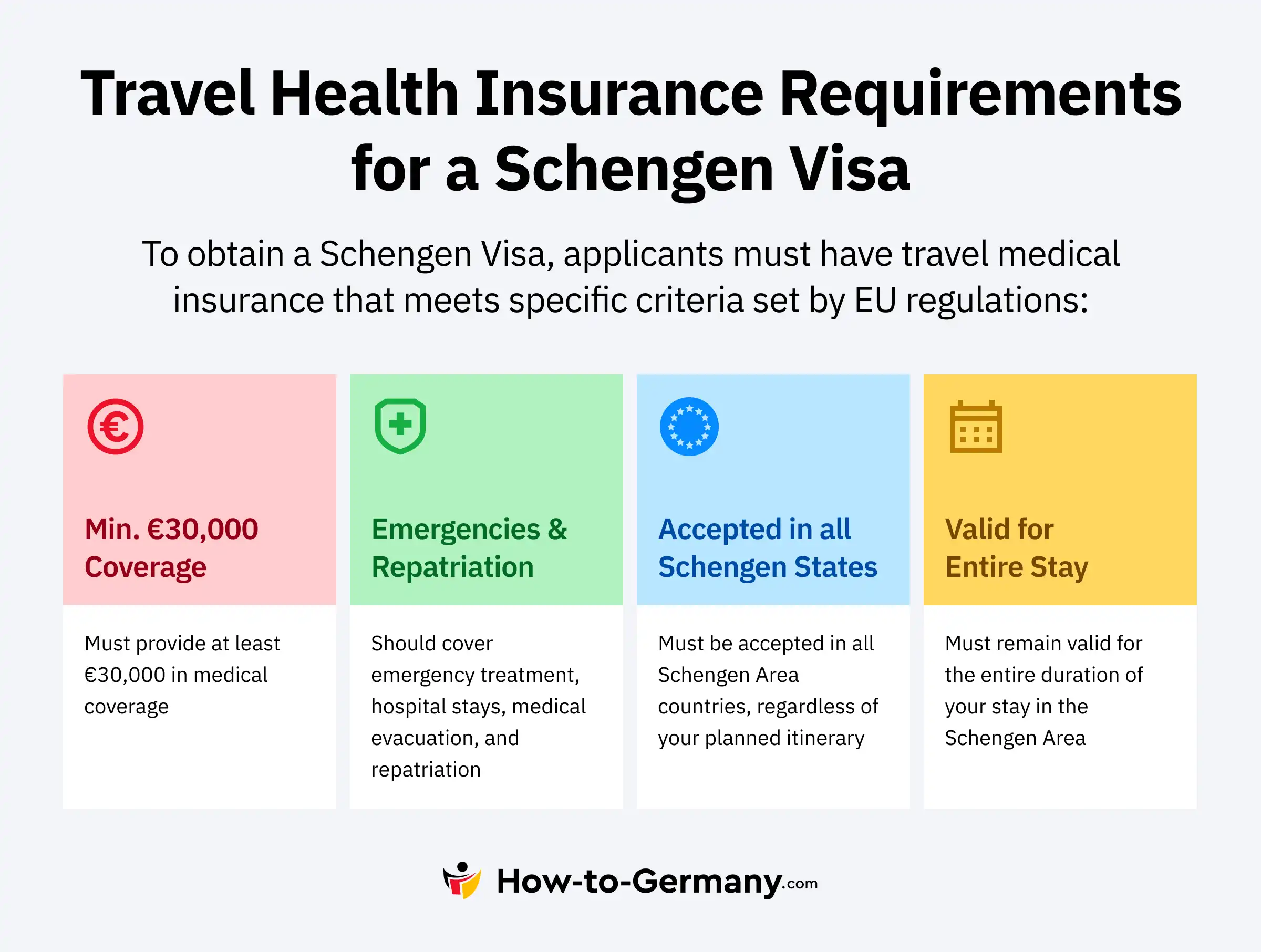

- Schengen travel insurance must be valid in all Schengen countries.

- Some policies offer optional extended country coverage, including the United Kingdom, Ireland, and Cyprus.

- The sum insured must be at least €30,000, covering emergency medical treatment, hospitalization, medical repatriation, and repatriation in case of death.

- The policy should usually have €0 deductible / no co-pay / no reimbursement-only structure. Some German missions explicitly reject policies with reimbursement, deductibles, or co-pays.

- The insurance certificate should clearly show the insured person’s name, coverage dates, Schengen-wide validity, minimum coverage amount, and required emergency/repatriation benefits.

- The cost of a Schengen insurance policy depends on the provider, tariff, age, and stay length. Budget providers can start around €0.80–€1.10 per day, but minimum fees and senior pricing can make short stays or older applicants more expensive.

- Visa-exempt travelers from more than 60 countries do not need a Schengen visa for short stays, but ETIAS is expected to start in late 2026.

Schengen visa insurance is checked before your visa is issued

Schengen visa insurance is one of the documents most likely to delay a visa application if the certificate is unclear. The embassy does not only check whether you bought travel insurance. It checks whether the policy meets the Schengen visa insurance rules.

Common insurance rejection traps

- Wrong insurer assumption: The policy does not always need to come from a German or European insurer. Many embassies accept local approved providers, as long as the insurance meets Schengen rules and claims are recoverable in a Schengen State.

- Wrong country coverage: The certificate must cover all Schengen States, not only Germany or your main destination.

- Wrong coverage amount: The minimum coverage must be at least €30,000.

- Missing repatriation wording: The certificate should mention medical repatriation and repatriation in case of death.

- Deductible, co-pay, or reimbursement-only policies: Keep this point high on your checklist. Some German missions explicitly state that no reimbursement, deductible, or co-pay is accepted. Policies that require you to pay upfront and claim reimbursement later, or policies with any deductible/co-pay, may be rejected by the consulate. Choose a €0 deductible policy with clear direct-coverage wording unless your embassy checklist clearly allows otherwise.

- Insufficient dates: The policy must cover the full intended stay or transit. Some providers allow applicants to add 15 extra days because Schengen visas can include a 15-day grace period, but embassy practice can vary. Check the exact mission checklist.

- Unclear certificate: The certificate should be in English, German, or the language accepted by the mission, and it should clearly show the insured person’s name, dates, countries, coverage amount, and emergency benefits.

Embassy insurance checklist

Before submitting your visa application, check that your insurance certificate clearly states:

- Coverage amount: at least €30,000.

- Coverage area: all Schengen States.

- Coverage dates: the full intended stay or transit.

- Deductible: €0 deductible / no co-pay / no reimbursement-only structure where required by the mission.

- Emergency care: urgent medical treatment and emergency hospital treatment.

- Insured person: full name matching the passport.

- Repatriation: medical repatriation and repatriation in case of death.

- Visa wording: wording showing the policy is suitable for a Schengen visa application.

This page gives general guidance for Schengen visa health insurance in 2026. Embassy checklists, accepted local insurers, certificate wording, deductible rules, and upload procedures can differ by country and visa center. Always check the German embassy, consulate, or visa center responsible for your application before buying a policy. For complicated visa refusals or unclear insurance acceptance, consider getting advice from a qualified immigration lawyer or visa specialist.

Schengen visa insurance requirements and coverage

The German and European embassies will only accept a health insurance policy for the issuance of a Schengen visa if the following requirements are met:

- Coverage for all emergency medical expenses

- Coverage for the entire duration of the trip or transit

- Guaranteed return transportation or repatriation in the event of serious illness or death

- Minimum insurance coverage of at least €30,000 for each insured person

- No deductible, co-pay, or reimbursement-only structure where the embassy checklist prohibits it

- Policy issued by an insurer accepted by the relevant embassy or visa center

- Valid for the entire Schengen area

Schengen rules do not always require a German or European insurance company. Applicants are generally expected to take out insurance in their country of residence. If this is not possible, they can obtain insurance in another country, as long as claims against the insurer are recoverable in a Schengen State. Many German embassies also publish country-specific lists of accepted local providers.

Insurance benefits

A Schengen insurance plan covers only acute illnesses and accidents. The insurance includes these benefits:

- Costs for doctor’s visits, outpatient treatment, and prescription drugs

- Costs for hospitalization

- Medically necessary return transportation to the home country

- Repatriation of mortal remains in the event of death

Schengen visa insurance generally does not cover pre-existing conditions or planned medical treatment. Policies only cover emergency medical costs.

Even if a policy technically offers enough medical coverage, the embassy may reject it if the certificate shows a deductible, co-pay, or reimbursement-only setup. Some German missions state this directly in their medical insurance checklists. For visa applications, choose a policy that clearly shows no deductible, no co-pay, and direct coverage for emergency medical treatment, hospitalization, medical evacuation, and repatriation.

Country Coverage

Your Schengen visa insurance must cover all Schengen countries.

However, depending on the policy, coverage may extend to stays in other European countries, such as the United Kingdom, Ireland, and Cyprus.

Coverage for other European countries such as Albania, non-Schengen Balkan countries, or Turkey is generally excluded unless the policy includes broader European or worldwide coverage.

Additional services

You can take out Schengen visa insurance as pure travel health insurance or a combined policy with other travel insurance. Optional components are, for example:

- Insurance in the event of flight delays

- Insurance in the event of lost or stolen baggage

- Travel accident insurance

- Travel cancellation and curtailment insurance

- Travel liability insurance against the financial consequences of personal injury as well as financial and property damage

Additional travel insurance does not influence the issuance of a Schengen visa. The only relevant insurance for this is travel health insurance with sufficient medical and repatriation coverage.

Taking out Schengen visa insurance

You must take out Schengen visa insurance before applying for a visa. There are different options for doing this:

- You can purchase the policy online from an insurance provider of your choice.

- You can use an approved local insurer from the list published by the relevant embassy or visa center, if such a list exists in your country.

- If you book an organized trip to Europe through a travel agency, you can often purchase travel health insurance as part of the package. However, you should check such offers thoroughly and compare them with the conditions for Schengen insurance on the open market, as they are typically pricier.

- In some cases, European embassies work with subsidiaries of European insurance companies in your home country so that you can purchase the policy locally. However, these policies are not always the cheapest available either.

Buying Schengen visa insurance online

If you want to buy insurance for your Schengen visa application online, follow these steps:

- Check your embassy or visa center checklist first.

- Compare suitable offers, including local approved insurers if your embassy publishes a list.

- Select a policy that covers all Schengen countries, the full intended stay, at least €30,000, emergency medical treatment, hospitalization, and repatriation.

- Choose €0 deductible / no co-pay / no reimbursement-only structure if required by the mission.

- Fill out the online form of the provider of your choice. You will be asked for your data and information about the duration and destinations of your trip.

- Download the insurance certificate and check the wording before submitting it with your visa application.

Your insurance certificate will usually be emailed as a PDF file, or you can download it from the insurance company’s customer area. You must usually enclose printed copies in your visa application, unless your visa center or embassy uses a different digital upload process.

Claiming benefits from Schengen insurance

Your insurance certificate is also your proof of insurance for doctors and hospitals. Some insurance companies additionally issue you with a health card. You must present the certificate or card if you need medical treatment during your European trip.

The settlement of insurance claims varies. Hospitals usually bill the insurer directly. For outpatient treatment, you may have to pay the bill yourself initially and then get it reimbursed by your insurance company later. Enclose all medically confirmed treatment documents and prescriptions for medication with the reimbursement request.

You should report emergency medical treatment to the insurer immediately to avoid losing your entitlement to benefits. You can make such insurance reports 24/7 via the emergency hotline.

Costs for Schengen visa insurance

The costs for travel insurance depend on various factors:

- Age: Senior travelers usually pay a higher premium for Schengen travel insurance. For example, Dr-Walter / Provisit Visum charges €1.10 per day for travelers up to 64 years old, but €6.50 per day for travelers aged 65 or older.

- Duration of travel: Schengen travel insurance is often charged daily or by trip duration. Budget visa-compliant policies can start around €0.80–€1.10 per day, but minimum fees can make very short stays more expensive than the daily rate suggests.

- Minimum fees: Some providers apply a minimum premium. Dr-Walter / Provisit Visum, for example, has a €20 minimum fee, so a short trip will not necessarily cost only €1.10 multiplied by the number of travel days.

- Provider and tariff: AXA BASIC starts at €4.90 per day for 1–2 day stays, while the average daily cost decreases for longer trips.

- Sum insured and additional benefits: In addition to standard policies with a minimum coverage of €30,000, policies with higher coverage amounts are also offered. Rates with higher coverage amounts and additional benefits are typically pricier than standard rates.

Best providers for Schengen visa insurance

The following offers for Schengen visa insurance are particularly relevant because they are designed for Schengen visa applications and provide quick insurance certificates.

| Provider | Typical Coverage | Approximate 2026 Cost | Good For | Main Caution |

|---|---|---|---|---|

| AXA Schengen | €30,000 to higher premium coverage, depending on plan | BASIC starts at €4.90/day for very short stays; lower average per day for longer stays | Travelers who want a well-known Schengen-focused provider and immediate certificate | Not a €1.10/day provider for short stays |

| Dr-Walter / Provisit Visum | Schengen visa insurance with health-only or combined options | €1.10/day up to age 64; €6.50/day from age 65; €20 minimum fee | Budget-conscious applicants under 65 needing a visa-compliant German provider | Senior travelers and short-stay travelers can face much higher effective costs |

| EKTA | Budget travel medical policies, depending on selected plan | Often marketed around €0.80–€1.10/day for basic cover | Very price-sensitive applicants | Check embassy acceptance, deductible, and certificate wording carefully |

| Europ Assistance | Schengen and Schengen Plus options with extended country coverage | Depends on route, age, stay length, and tariff | Applicants wanting a recognized travel assistance brand | Check whether the certificate names all Schengen requirements clearly |

- AXA Schengen: Offers several tariffs, including Basic, Essential, Premium, and annual options. Basic starts at €4.90 per day for very short stays, with lower average daily pricing for longer trips.

- Dr-Walter / Provisit Visum: Offers health insurance only or combined cover with accident and liability insurance, often used for Schengen visa applications. The advertised €1.10 daily rate applies to travelers up to age 64, but the minimum fee is €20. From age 65, the health-only rate rises to €6.50 per day.

- EKTA: A budget option that may suit applicants looking for bare-minimum pricing, but the certificate and deductible wording should be checked carefully against the embassy checklist.

- Europ Assistance: Offers Schengen and Schengen Plus options with extended country coverage such as the UK, Ireland, and Cyprus.

Schengen area and Schengen visa

The Schengen Agreement was concluded in 1985 and has since been gradually expanded. Citizens of the Schengen member states enjoy freedom of travel and settlement throughout the entire Schengen zone.

The Schengen zone includes all European Union countries except Ireland and Cyprus. Iceland, Norway, Switzerland, and Liechtenstein are also Schengen countries. Since 1 January 2025, Bulgaria and Romania have been full Schengen members after checks at internal land borders were lifted. This means days spent in Bulgaria or Romania now count toward the Schengen 90 days in any 180-day period limit.

Older internet guides may still describe Bulgaria and Romania as partial or non-Schengen cases. That is outdated for 2026. They are now full Schengen members, so visa-free travelers and Schengen visa holders must count days spent there toward the rolling 90/180-day Schengen limit.

The United Kingdom is neither an EU nor a Schengen member state

The United Kingdom left the EU in 2020 and never joined the Schengen Agreement. Therefore, travel to the United Kingdom is not covered by a Schengen visa. Depending on nationality, travelers may need a separate UK visa or UK electronic travel authorization.

Schengen visa — for free travel in all Schengen countries

Visas issued by the embassies of Germany or another Schengen country are generally valid for the entire Schengen zone. The rules for issuing visas are standardized in all Schengen member states.

Schengen visa types

Schengen visas come in 2 types: C-visas and D-visas. The type of visa you need depends on the duration and purpose of your stay:

- C-visas allow the holder to travel within the Schengen area for up to 90 days within 180 days. They are issued for single, double, or multiple entries. This type of visa is suitable for tourist trips, visits to friends and family, and short-term business or study trips.

- D-visas are national visas for long-term stays in a Schengen country. If you plan to stay in the country for more than 90 days, you will need this type of visa. The validity of a D-visa and the residence permit issued on its basis depends on the purpose of the trip. In addition to tourist or personal travel reasons, these may include, for example, student visas, work visas, or visas for job seekers.

Schengen visa requirements

Visa applicants can obtain short-stay Schengen visas only with Schengen visa insurance. A visa will not be issued without valid travel medical insurance, and the policy must meet the minimum requirements of the Schengen member states.

In addition, applicants for a Schengen visa must fulfill certain other visa requirements. These include a plausible reason for travel, proof of willingness to return, and evidence of financing for the trip through their financial resources or a declaration of commitment from an inviting person to cover all costs. If you apply for your visa at a German embassy, the person invited must have a main residence in Germany.

Visa and health insurance obligations in the Schengen zone

Regarding visa requirements for Germany and Europe and, consequently, the obligation to take out travel health insurance, 3 groups of international travelers can be distinguished:

- Citizens of Schengen countries: They do not need a visa or special Schengen visa insurance for travel within the Schengen zone. Their home country’s health insurance usually covers emergency medical expenses. EU citizens with statutory health insurance can claim medically necessary treatment in the Schengen zone through the European Health Insurance Card (EHIC).

- Citizens of visa-exempt countries: They do not need a Schengen visa or mandatory Schengen visa insurance for a stay of up to 90 days in any 180-day period. The EU has visa-free arrangements with more than 60 non-EU countries and territories, including the United Kingdom, the United States, Canada, Australia, New Zealand, Japan, Brazil, Singapore, and South Korea. Travel health insurance is still strongly recommended.

- Travelers from visa-required countries: They require a Schengen visa and Schengen visa insurance.

ETIAS is expected to start in the last quarter of 2026. It is not a Schengen visa and does not replace travel health insurance. It is a travel authorization for visa-exempt travelers entering participating European countries for short stays. Visa-required travelers will continue to apply for a Schengen visa instead.

Conclusion

Schengen visa insurance is mandatory for travelers from visa-required countries entering the Schengen area. It ensures coverage for emergency medical treatment, hospitalization, medical repatriation, and repatriation in case of death. Policies must meet standardized requirements, including minimum coverage of €30,000, validity throughout all Schengen countries, and coverage for the full intended stay.

The most important correction is that the insurance does not always need to be purchased from a German or European company. Many embassies accept approved local providers in the applicant’s country of residence, as long as the certificate meets Schengen rules and claims are recoverable in a Schengen State. Applicants should also avoid common rejection traps: unclear certificate wording, missing repatriation benefits, wrong country coverage, deductibles, reimbursement-only structures, or insufficient travel dates.

Visa-exempt travelers from more than 60 countries do not need Schengen visa insurance as a visa document, but travel insurance is still strongly recommended. From late 2026, ETIAS is expected to become relevant for visa-exempt short-stay travelers. Bulgaria and Romania are now full Schengen members, so time spent there counts toward the rolling 90/180-day Schengen limit. By carefully comparing providers, checking the embassy-specific insurance checklist, and choosing a policy with clear Schengen-compliant wording, travelers can avoid unnecessary delays and submit a stronger visa application.

Frequently Asked Questions — FAQ

The insurance conditions are decisive here. Travel medical insurance for the Schengen area can be taken out for a single entry, multiple trips, or annual insurance with any number of entries to Europe. The number of entries you require also depends on what type of Schengen visa you are applying for.

Insurers offer Schengen travel insurance with and without renewal options. Renewal is usually not possible in standard plans. In contrast, there is an extension option for tariffs with more comprehensive coverage.

If your Schengen visa is rejected, the insurance premium will be refunded. To achieve this, you must submit the embassy’s rejection notice to your insurance company.

Yes. All providers of Schengen insurance offer the option of early cancellation if you have to cut your trip short. The cancellation will take effect as soon as your insurer receives it. Any overpaid premiums will be refunded.