How we earn our money

We finance our services on how-to-germany.com through affiliate programs.

When a user orders a financial product through our site and their application is approved, we may receive a commission from some providers. It’s important to note that this does not in any way influence our independent ratings and recommendations.

All the products we present on how-to-germany.com are selected for their quality, range of services, and excellent value for money.

VAT in Germany

Written by

Janine El-Saghir

Janine El Saghir is an editor at How-to-Germany.com, where she specializes in the practical aspects of daily life and integration for expatriates. With years of...

Written by

Janine El-Saghir

Janine El Saghir is an editor at How-to-Germany.com, where she specializes in the practical aspects of daily life and integration for expatriates. With years of...

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

- Standard VAT rate: Germany’s regular VAT rate is 19%.

- Reduced VAT rate: A 7% rate applies to selected goods and services, such as many groceries, books, newspapers, local public transport, and hotel stays.

- Small business rule: Since 2025, the Kleinunternehmerregelung applies if previous-year turnover did not exceed €25,000 net and current-year turnover does not exceed €100,000 net.

- VAT filing: VAT returns are usually filed quarterly, monthly, or annually depending on the previous year’s VAT liability.

- VAT ID: The German VAT ID is the Umsatzsteuer-Identifikationsnummer, or USt-IdNr., and follows the format DE123456789.

- E-invoicing: Since 2025, B2B e-invoicing rules apply in Germany, with transition periods for issuing structured electronic invoices.

What is VAT?

One might wonder about the name “VAT”. Though consumers don’t receive any direct benefit by paying an additional 7% or 19% on top of the net price, the name stems from the value added principle in effect since 1968. According to this principle, businesses pay VAT only on the added value achieved. This added value represents the difference between your purchase price and the sales price the end customer pays.

In Germany, smaller businesses can opt to be exempt from charging VAT under the small business regulation, known as the Kleinunternehmerregelung. In this case, they issue invoices without VAT, but they also cannot reclaim input tax on their own business purchases. Essentially, if a business does not charge VAT to customers and does not pay VAT to the tax office, it also cannot report previously paid VAT as input tax and claim a refund.

German VAT Rates

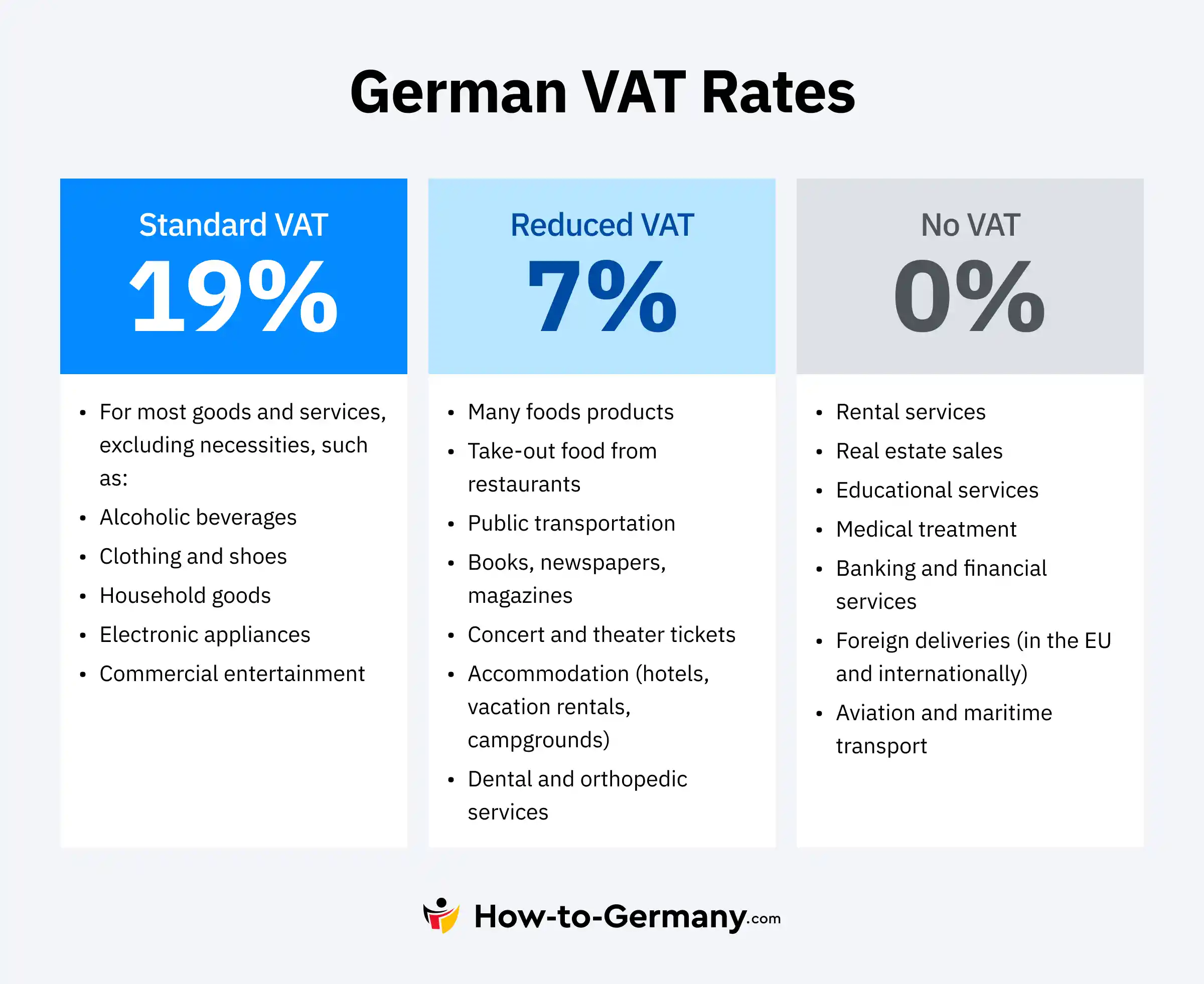

German tax law specifies three distinct VAT rates. The most common, known by most consumers, is the 19% rate. Some goods and services, however, benefit from a reduced rate of 7%. This lower rate is designed to alleviate the financial impact on consumers for certain essential purchases. Some businesses also use an average-rate VAT system for specific agricultural and forestry businesses, although this is less common.

The applicable rate often depends on the nature of the service or product provided. To illustrate, beverages are generally taxed at 19%, the standard VAT rate. However, milk, being a food item, is only taxed at 7%. Surprisingly, despite being a basic necessity, mineral water is taxed at 19%.

The 7% reduced rate applies to items such as:

- Books

- Copyrighted services, including articles and graphics

- Entry to concerts, theaters, and museums

- Local public transport

- Magazines

- Newspapers

- Performances by artists

- Some groceries

- Stays at hotels or campsites

- Take away food

Certain services and transactions are exempt from VAT, including:

- Medical treatment and nursing services

- Real estate rentals and leasing

- Real estate sales

| VAT Treatment | Rate | Typical Examples | Important Note |

|---|---|---|---|

| Reduced rate | 7% | Many groceries, books, newspapers, local public transport, hotel stays | The exact rate depends on the product or service category. |

| Standard rate | 19% | Most goods and services, many drinks, electronics, consulting services | This is the default VAT rate in Germany. |

| VAT-exempt | 0% | Some medical services, real estate sales, long-term real estate rentals | VAT exemption does not always mean input tax can be reclaimed. |

German VAT Number

Known as the VAT ID in English, the Umsatzsteuer-Identifikationsnummer (USt-IdNr.) in German serves as an identification number for businesses involved in cross-border VAT matters, especially intra-EU transactions. It follows the format DE123456789.

It is essential to distinguish this from the general German tax number, known as the Steuernummer. The Steuernummer is issued by the local tax office and is often used for domestic tax matters and invoices. The USt-IdNr., by contrast, is the VAT identification number used for EU business transactions.

VAT or Sales Tax?

For entrepreneurs, tradespeople, self-employed individuals, freelancers, and service providers, what we call VAT is synonymous with sales tax, known in German as Umsatzsteuer (USt.).

Both terms, “VAT” and “sales tax,” describe the same concept. The preference for the term “sales tax” over “VAT” in some contexts arises because there exists a sales tax law (UStG) in Germany, but no specific law named after value-added tax (VAT). Both terminologies denote the indirect tax added to the value of a product, and all businesses are required to transfer the respective amount to the tax office.

VAT splits into two categories: sales tax and input tax. When a business sells a product or service, it charges sales tax, which the customer pays. Conversely, when you, as a business owner, purchase an item from a vendor, you pay input tax, known in German as Vorsteuer. If you are subject to regular VAT rules, this input tax can usually be deducted from the VAT you owe to the tax office.

VAT Returns for Entrepreneurs

If you’re an entrepreneur in Germany, you’re also subject to taxation. You must declare the tax amount to the responsible tax authority and ensure its payment. This entails submitting preliminary VAT returns to the tax office, a requirement for many self-employed individuals, regardless of your business type, be it commercial or freelance.

Typically, VAT should be paid quarterly to the tax office. However, if your annual VAT liability for the previous year exceeds €9,000, preliminary VAT returns generally have to be filed monthly. On the other hand, if it is below €2,000, the tax office may exempt you from preliminary VAT returns, meaning an annual VAT return is usually sufficient.

Start-ups or new businesses are not automatically required to report VAT monthly for their first and second year if they were founded between 2021 and 31 December 2026. During this transition period, start-ups generally follow the standard VAT filing rules, which usually means quarterly reporting unless the actual or estimated VAT liability requires a different filing frequency. However, the tax office can still set the filing frequency depending on the case.

Furthermore, by the year’s end, business owners must provide a comprehensive VAT return. This document, submitted alongside the income tax return, acts as a reconciliation for the tax office, offsetting VAT already paid against the total tax amount due.

VAT returns and preliminary VAT returns are usually submitted online via ELSTER. For structured B2B e-invoicing rules, businesses can also consult the Federal Ministry of Finance e-invoicing FAQ.

Save Money with the Small Business Regulation

The small business regulation is a specific rule concerning VAT. Under this guideline, companies with sales that don’t surpass a predetermined threshold are exempt from charging VAT. Therefore, this means that start-ups and small enterprises won’t have to charge VAT if their revenue remains below this set limit.

To be eligible for the small business regulation from 2025 onward, two criteria need to be met:

- The company’s net annual turnover for the previous year did not exceed €25,000.

- The company’s net annual turnover for the current year does not exceed €100,000.

The current-year limit is no longer just a forecast. If your turnover exceeds €100,000 during the year, the small business regulation stops applying from the point the limit is exceeded, and you must start charging VAT from that transaction onward.

Once you opt out of the small business regulation and choose regular VAT taxation, you’re generally bound by that decision for a span of five years. Hence, it’s crucial to forecast your business’s trajectory with accuracy. For many new businesses, a turnover exceeding €100,000 may initially seem ambitious. However, depending on your company sector, this threshold might be achievable faster than anticipated. On the other hand, if you’re pursuing a side business, you could remain under this cap for an extended period. So, it’s wise to evaluate your future business potential thoroughly before committing to regular VAT taxation.

New businesses should be aware that some clients or customers in certain sectors may be hesitant to engage with a small business entity. There’s a perception that such companies might lack the required experience or professionalism. And since clients won’t be charged VAT for your services, they can’t deduct VAT from their expenses.

For clarity, when issuing an invoice without VAT as a small business operator in Germany, use a German legal reference, not the Austrian Section 6 (1) Z 27 UStG. A standard German invoice note is: “Gemäß § 19 UStG wird keine Umsatzsteuer berechnet.”

Use this simple check before issuing invoices without VAT:

- Previous year: Was your German net turnover €25,000 or less?

- Current year: Will your actual German net turnover stay at or below €100,000?

- Invoice wording: Does your invoice mention § 19 UStG instead of charging VAT?

- Input tax: Are you comfortable not reclaiming VAT on business expenses?

- B2B clients: Are your clients okay receiving invoices without deductible VAT?

If you answer “yes” to all points, the small business regulation may fit your situation. If you expect high start-up costs, mostly B2B clients, or turnover above the limit, regular VAT taxation may be more practical.

B2B E-Invoicing Rules Since 2025

Germany introduced new B2B e-invoicing rules from 1 January 2025. These rules mainly affect transactions between domestic businesses. For VAT purposes, a simple PDF invoice is no longer considered a structured e-invoice under the new definition. Valid e-invoice formats must allow electronic processing, such as XRechnung or ZUGFeRD.

There are transition periods, so not every business must immediately issue structured e-invoices in every case. However, businesses should be technically able to receive e-invoices and should check whether their invoicing software supports compliant formats. This is especially important for freelancers, consultants, agencies, and small businesses that invoice German business clients.

Kleinunternehmer are excluded from some e-invoicing issuing obligations for their own small-business invoices. However, if they work with German business clients, they should still understand how e-invoices are received, stored, and handled in accounting software.

EU Small Business Rules for Cross-Border Sales

Since 2025, the small business scheme has also become more relevant for cross-border EU activity. Under the new EU SME scheme, eligible small businesses may be able to use small-business VAT relief in other EU countries if they meet the relevant turnover limits and reporting requirements.

This matters for expats in Germany who sell digital services, consulting, design, writing, or other services to clients in other EU countries. The German Kleinunternehmerregelung does not automatically remove all EU VAT obligations. Depending on the customer, service type, and country, you may still need a VAT ID, reverse-charge wording, special reporting, or separate registration.

Frequently Asked Questions

Partially tax-free turnover refers to businesses that have both taxable and non-taxable sales. In contrast, exclusively tax-free turnover means all the business’s sales are non-taxable under VAT system regulation.

When selling to customers within the European Union, the reverse-charge system can apply. This system means that the buyer, instead of the seller, is responsible for the VAT. Always check with the tax office to ensure you’re following European VAT regulations correctly.

The prior tax deduction system allows businesses to deduct vat they’ve paid on business-related purchases from their vat obligation. This ensures that only the end consumer bears the final cost of the VAT.

Yes, if your business deals with selling properties, you need to be aware of the property pre-tax deduction. However, there are certain tax exemptions related to property transactions, such as residential sales.

Yes, foreign companies that generate taxable turnover in Germany may become a VAT obligated company. It’s crucial for such companies to understand their VAT obligation when trading within Germany.

For foreign events managers or companies supplying services from outside Germany to German consumers, the VAT system regulation requires them to consider vat rates applicable in Germany. It’s especially crucial for electronically supplied services or one off seminar events in Germany from foreign businesses.