How we earn our money

We finance our services on how-to-germany.com through affiliate programs.

When a user orders a financial product through our site and their application is approved, we may receive a commission from some providers. It’s important to note that this does not in any way influence our independent ratings and recommendations.

All the products we present on how-to-germany.com are selected for their quality, range of services, and excellent value for money.

Income Tax Classes in Germany

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Reviewed by

Erkan Boga

Erkan Boga is the founder and CEO of qmedia GmbH, the publishing house behind How-to-Germany.com. He established the platform with the clear vision of creating...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

Edited by

Sadie Voss

Content Lead & Editor

Sadie Voss is the Lead Editor for How-to-Germany.com. As an expat who carved her own way into Berlin from the United States, Sadie is deeply...

- Germany has six wage tax classes: Tax classes 1 to 6 determine how much wage tax your employer withholds from your monthly salary.

- Your tax class does not decide your final annual tax bill: It mainly affects monthly payroll deductions. Your final tax liability is calculated in your annual income tax return.

- Single employees are usually in tax class 1, while single parents can qualify for tax class 2 if they meet the requirements.

- Married couples can usually choose between 4/4, 4/4 with factor, or 3/5. Tax classes 3 and 5 remain valid in 2026 despite political debate about future reforms.

- Tax class 6 applies to second jobs and usually has the highest monthly deductions because no basic allowance is applied there.

- The deadline to change tax class is usually November 30 if the change should still apply for the current tax year.

Understanding the Different German Tax Classes

The income tax bracket you are assigned depends primarily on your marital status. Under certain circumstances, married couples can change their income tax class to improve monthly cash flow and avoid large tax refunds or back payments. Here, you can learn everything about the wage tax classes, how they affect your payslip, and which tax class usually applies to your situation.

You can check the legal basis for wage tax classes in the German Income Tax Act, submit tax-class changes through ELSTER, and find federal tax guidance through the Federal Ministry of Finance.

What is meant by the wage tax class?

The amount of tax deducted from your wages depends on your tax bracket. Someone in wage tax class 1 has a different monthly tax deduction than a taxpayer in wage tax class 2.

The tax class is entered as a wage tax deduction feature on your wage tax card. Today, the wage tax card is only available in electronic form. The tax class is, therefore, stored as ELStAM at the tax office. ELStAM stands for Elektronisches Lohnsteuer-Abzugsmerkmal and is the most important criterion for the amount of wage tax your employer withholds from your salary.

Your German tax class does not create a separate tax rate for your final annual income tax. It mainly controls how much wage tax is withheld from your monthly payslip. After the end of the year, your actual income tax is calculated through the annual tax return. If too much was withheld, you may receive a refund. If too little was withheld, you may have to pay back taxes.

Which wage tax classes are there?

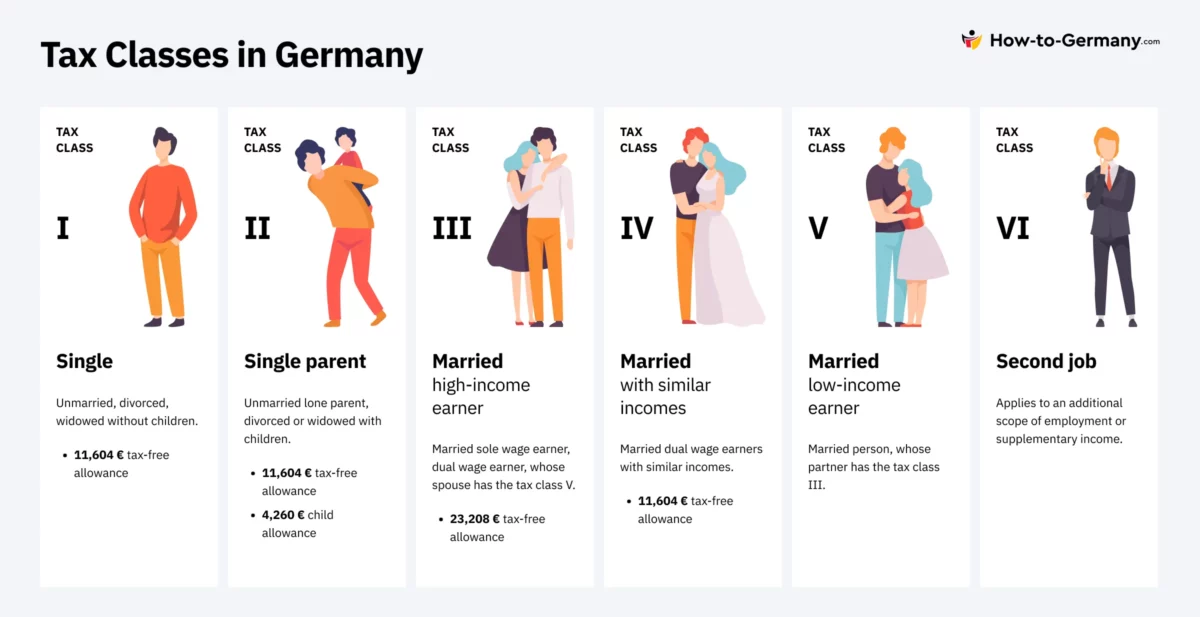

There are a total of six different wage tax classes (wage tax classes 1 to 6) for wage and income tax in Germany. The individual wage tax classes differ primarily regarding marital status. In addition to the wage tax class, the amount of income is an essential criterion for the amount of taxes. Within a wage tax class, a taxpayer with a low income will pay less tax than someone with a high income. This ensures tax fairness, as so-called high earners pay more taxes than low earners.

| Tax Class | Usually Applies To | Main Effect |

|---|---|---|

| Tax class 1 | Single, divorced, permanently separated, or widowed employees after the transition period | Standard tax class for unmarried employees without single-parent relief |

| Tax class 2 | Single parents who qualify for the single-parent relief amount | Lower monthly withholding because the single-parent relief is considered |

| Tax class 3 | Married partner with significantly higher income, usually paired with tax class 5 | Lower monthly withholding for the higher earner |

| Tax class 4 | Married couples with similar incomes | Similar to tax class 1 for each spouse; often balanced for equal incomes |

| Tax class 4 with factor | Married couples who want more accurate monthly withholding | Applies the splitting advantage more evenly and can reduce back payments |

| Tax class 5 | Married partner with lower income, paired with tax class 3 | Higher monthly withholding for the lower earner |

| Tax class 6 | Employees with a second or additional job | Highest withholding because basic allowances are already used in the first job |

Single with no children? You are usually in tax class 1.

Single parent with a child in your household? You may qualify for tax class 2.

Married with similar incomes? Tax class 4/4 is usually the standard option.

Married with one much higher income? Tax class 3/5 can increase monthly net income for the higher earner but may cause back payments.

Married and want fewer surprises? Tax class 4 with factor is often the most balanced option.

Working a second job? The second job is usually taxed in tax class 6.

Classification into tax classes

In tax class 1 belong single, from their spouse separated living or already divorced employees. In a pending divorce, spouses must each register in tax class 1 if the joint residence is abandoned and two separate residences already exist.

The tax class 2 applies to single parents, provided that they are entitled to the relief amount for single parents. The tax office automatically takes the relief amount into account for the first child if the requirements are met. If a single parent has more than one child, the additional relief amount must usually be applied for separately at the local tax office.

In tax class 3 are spouses classified, who earn significantly more than the partner. The partner with the lower income is placed in tax class 5 as compensation. The combination of tax classes 3 and 5 is still valid in 2026 and can still be used by married couples and registered civil partners. It remains especially relevant when one spouse earns much more than the other.

Today, tax class 4 is automatically specified if both spouses are employed. Provided that there is no significant difference in the amount of income, this tax class combination is usually the most balanced. In tax class 4 there is a special feature: it can be selected with factor. This means that the tax office applies the advantage of spousal splitting more accurately during the year. The factor method helps distribute monthly wage tax more fairly between both spouses and can reduce the risk of back payments.

The tax class 5 applies to spouses with the lower income; it is the counterpart to tax class 3.

In tax class 6 you will be taxed if you have two jobs subject to wage tax. In this case, one job is registered in wage tax class 6. Since this is a second income and the basic allowance is already considered in the first job, the deductions in tax class 6 are quite high.

The possible abolition of tax classes 3 and 5 has been heavily debated in recent years. A reform plan discussed moving married couples toward tax class 4 with factor in the future. However, tax classes 3 and 5 remain fully valid and active in 2026. Married couples do not need to switch away from 3/5 unless another combination suits their monthly cash flow better.

What wage tax class combinations are there for married couples?

Basically, spouses are taxed together if that is the more favorable option for you. For the deduction of the wage tax, however, only the respective own wage is always applied. At the end of the year, both incomes are combined so that the tax for the entire year results. As a consequence, it is almost impossible to avoid paying too much or too little tax during the year. This can result in a substantial back tax payment in the coming year. To avoid this, spouses can choose between two combinations of tax classes or make use of the factor method.

The combination that you have chosen once for yourself and your partner will continue to apply unchanged in the coming year — provided that the legal requirements continue to be met. The factor procedure in tax class 4 is generally valid for two years. It should be applied for again if your income, employment, or household situation changes significantly.

A change from the tax class combination 3 and 5 to 4 and 4, or to 4 and 4 with factor, must be applied for at the tax office. The easiest way to make the change is through ELSTER or by submitting the official form for tax class changes for spouses and registered civil partners.

If you change the tax class, the tax office sets a deadline for this. At the latest on 30 November of the year the application must be at the tax office to apply for the change for the current year. The tax office will then change your tax class in the ELStAM system so that the tax is calculated accordingly.

| Combination | Best For | Possible Downside |

|---|---|---|

| 3/5 | Couples where one partner earns much more than the other | Can lead to back payments and high deductions for the partner in tax class 5 |

| 4/4 | Couples with similar incomes | May not reflect the splitting advantage as accurately during the year |

| 4/4 with factor | Couples who want monthly withholding to match their real annual tax more closely | Requires an application and income estimates |

Suppose one spouse earns €5,000 gross per month and the other earns €1,800 gross per month. With tax class 3/5, the higher earner usually receives more net salary each month, while the lower earner receives less. This can improve household cash flow during the year, but it can also increase the risk of a tax back payment after filing the annual return. With 4/4 with factor, the monthly deduction is usually more balanced and closer to the final annual tax.

What’s the deal with child allowances?

In tax class 2 there is a relief amount for single parents. It is granted to single employees who have at least one child living in their household. For the child, there must be an entitlement to child benefit or there must be an allowance for children. To qualify for the relief amount, the child must live with the taxpayer or have a secondary residence.

The single-parent relief amount is €4,260 per year for the first child. For each additional child, €240 is added. This relief amount is separate from the child allowance and is intended to reduce the tax burden for single parents who live without another adult in the household.

The child allowance is to be distinguished from the relief amount. For the 2026 tax year, the combined child allowance is €9,756 per child. This consists of €6,828 for the child’s basic needs and €2,928 for care, education, and training. In practice, parents do not simply receive both child benefit and the child allowance as a double benefit. The tax office checks which option is more favorable as part of the annual tax assessment.

The single-parent relief amount reduces taxable income for qualifying single parents in tax class 2. The child allowance is a separate tax allowance for parents and is compared with child benefit during the tax assessment. These two rules serve different purposes and should not be mixed up.

Summary on the income tax bracket

Although it may seem relatively complex at first glance, the system of wage tax brackets is relatively easy to understand upon closer inspection. Your tax class mainly determines how much tax is withheld from your monthly salary, not your final annual tax burden.

Single employees are usually in tax class 1, single parents can qualify for tax class 2, married couples can choose between 3/5, 4/4, and 4/4 with factor, and second jobs usually fall into tax class 6. In 2026, tax classes 3 and 5 remain valid, the single-parent relief amount is €4,260 for the first child, and the combined child allowance is €9,756 per child.

Insofar as a choice of tax class is possible, you should carefully consider the alternatives. While it is not possible to make a blanket recommendation, there are certainly margins for maneuver. For married couples, the best choice often depends less on “saving taxes” and more on avoiding unpleasant back payments while keeping monthly household cash flow predictable.

FAQ

A tax class in Germany determines how much wage tax your employer withholds from your monthly salary. It does not decide your final annual tax bill. Your final tax liability is calculated after the end of the year through your income tax return.

If you are single, divorced, widowed, or permanently separated, you are usually assigned to tax class 1. If you are a single parent and meet the requirements for single-parent relief, you may qualify for tax class 2 instead.

Married couples usually choose between tax class 4/4, 4/4 with factor, or 3/5. Tax class 4/4 is often best for couples with similar incomes. Tax class 3/5 can increase monthly net income if one spouse earns much more, but it can lead to back payments. Tax class 4/4 with factor is often the most balanced option.

Yes. Tax classes 3 and 5 remain valid in Germany in 2026. Their possible abolition has been debated politically, but married couples can still use the 3/5 combination if they meet the requirements.

Changing your tax class usually does not reduce your final annual tax liability. It mainly changes how much tax is withheld from your monthly salary. This can improve monthly cash flow, but the final amount is corrected when you file your annual tax return.