How we earn our money

We finance our services on how-to-germany.com through affiliate programs.

When a user orders a financial product through our site and their application is approved, we may receive a commission from some providers. It’s important to note that this does not in any way influence our independent ratings and recommendations.

All the products we present on how-to-germany.com are selected for their quality, range of services, and excellent value for money.

Statutory Health Insurance in Germany

German Statutory Health Insurance: Essentials

- Health insurance is mandatory in Germany. Everyone must be insured either through statutory or private health insurance.

- The same regulations generally apply to expats with long-term residence as to German citizens.

- Employees with an income up to the compulsory insurance threshold of €77,400 (2026) must be insured in statutory health insurance; switching to private insurance is not permitted.

- Freelancers, the self-employed, and civil servants are not subject to compulsory statutory insurance and can choose between voluntary statutory insurance and private health insurance.

- Students can apply for an exemption from statutory insurance at the beginning of their studies and opt for private health insurance instead.

How does German Health Insurance Work?

Health insurance in Germany is divided into statutory and private health insurance. Statutory health insurance is the most important pillar of the health insurance system. 90% of all inhabitants are insured under a statutory health insurance scheme.

The Statutory Healthcare System in Germany

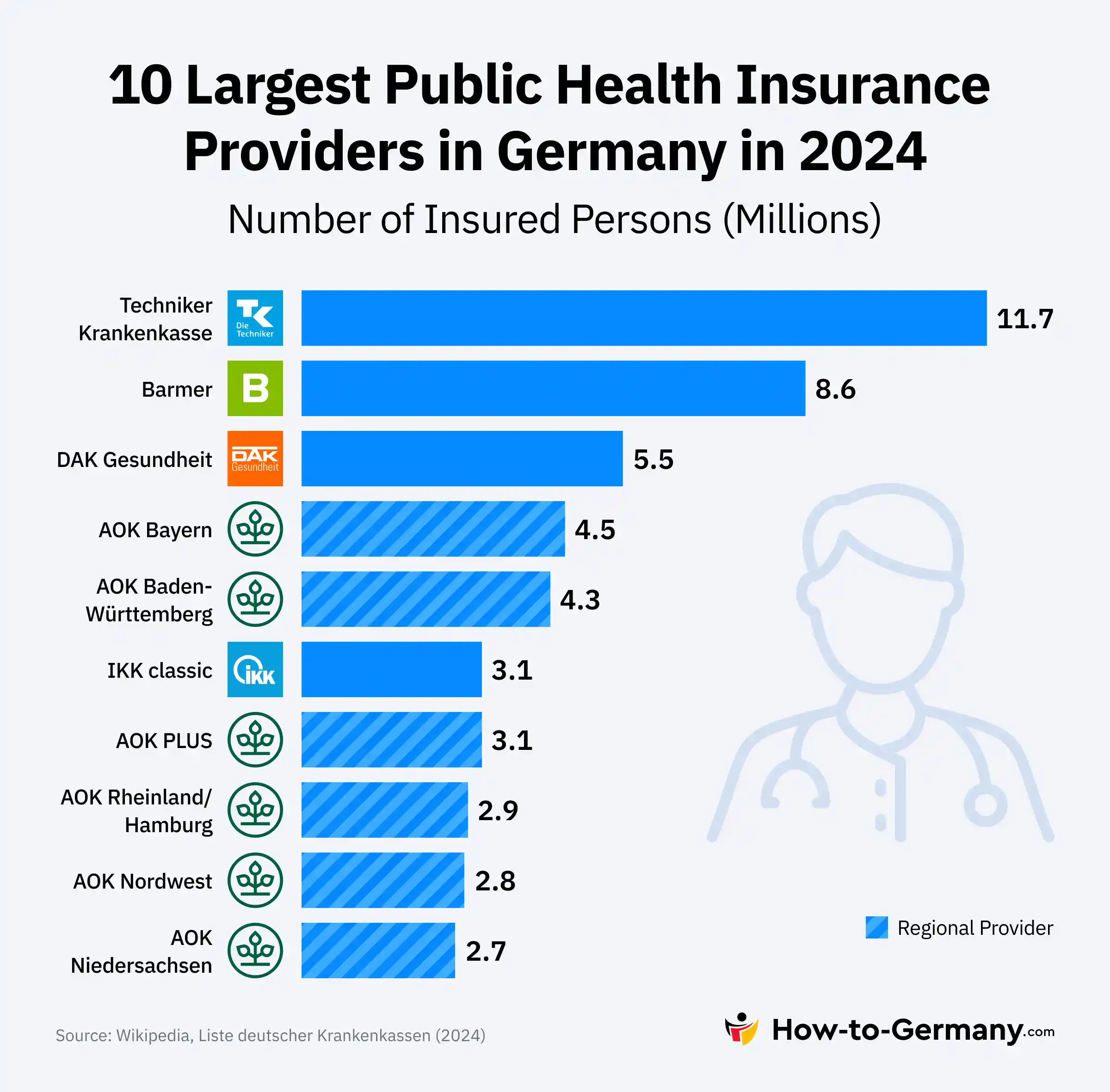

The foundations for today’s statutory health insurance in Germany were laid back in 1883 and became a model for many other countries. Today, people with public insurance can choose between 95 statutory health insurance funds.

Statutory health insurance providers are public, self-governing, non-profit organizations.

Public insurance in Germany is divided into three areas, but its benefits are identical: compulsory, voluntary, and non-contributory family insurance.

Compulsory Health Insurance

The compulsory insurance threshold for public insurance is adjusted annually. It currently (2026) stands at €77,400. Employees with a lower gross income must take out statutory health insurance. They must take out insurance with a statutory health insurance funds.

Voluntary Insurance with a Statutory Health Insurance Scheme

Employees with more than €77,400 (2026) limit income, freelancers, the self-employed, and civil servants can take out voluntary public health insurance or switch to private insurance.

Special regulations for students

Special regulations apply to students. Up to 30, they can take out statutory student health insurance at a particularly favorable rate. Subsequently, they can take out voluntary, statutory health insurance at higher premiums or change to a private insurance provider.

Alternatively, students can apply for an exemption from public insurance at the beginning of their studies and take out private insurance. Private insurers also offer special rates and favorable conditions for private students health insurance.

Non-Contributory Family Insurance Cover

Spouses and children can be insured free of charge if their income is below the marginal earnings threshold of currently €565 (2026) (mini-jobbers: €603). Students up to the age of 25 can also take advantage of non-contributory insurance.

Private Health Insurance in Germany

If you meet the requirements, you can take out private health insurance.

Private health insurance’s benefits and premium amounts depend on your chosen tariff. You conclude an individual contract with your private health insurance company. Your age, state of health at the start of insurance, and professional and personal risk profile determine the premium amount.

Private insurance offers a broader range of benefits than the statutory system and enables more adequate health insurance with customized tariffs. However, non-contributory insurance for family members is not possible with private health insurance.

What Regulations Apply to Health Insurance for Expats?

The same regulations apply to health insurance for expats with a residence permit of at least 12 months as for German citizens. As an expat, you can only take out private health insurance if you earn more than €77,400 (2026) per year as an employee, are a student, or work as a freelancer or self-employed person.

Some expats cannot take out public insurance. This concerns:

- Students in language and preparatory courses

- Visiting academics without a regular employment relationship with their German university

- People who currently have no health insurance and were previously privately insured in Germany

- Freelancers and self-employed individuals who take out health insurance in Germany for the first time

EU citizens and expats from Iceland, Liechtenstein, Norway, and Switzerland can also receive medical treatment in Germany with the European Health Insurance Card (EHIC). However, the card is not a permanent substitute for comprehensive health insurance.

Private health insurance providers such as ottonova and Feather offer special expat insurance to students and other expats living in Germany temporarily (maximum 5 years).

What Benefits does Statutory Health Insurance Offer?

You can claim all relevant health benefits if you opt for public insurance. Statutory health insurance coverage includes:

- Outpatient medical treatment (general practitioner and specialists)

- Hospital treatment

- Psychotherapy

- medication

- Remedies — for example, physiotherapy or speech therapy

- Auxiliary aids — for example, wheelchairs, prostheses, and visual aids

- Preventive medical check-ups (for certain illnesses, with age limits)

- Dental treatment, dentures

- Orthodontics (up to the age of 18, higher degrees of severity only)

- Medical rehabilitation (if not covered by pension insurance)

However, statutory health insurance benefits are limited to medically necessary and cost-effective treatments. The system only covers standard benefits; insured people must pay for all other therapies.

Patients with public insurance must make co-payments for many medical services. They are particularly high for dentures and certain dental treatments, as statutory health insurance dentists must always choose the most cost-effective treatment option. Dental health insurance is available for additional coverage.

Does German Statutory Health Insurance Coverage Apply Abroad?

The European Health Insurance Card (EHIC) allows you to use public healthcare services within the EU and in Iceland, Liechtenstein, Norway, and Switzerland.

To travel to other countries, you will need travel insurance, for which you can find affordable offers from many insurers.

Privately insured patients generally have worldwide insurance coverage through their private health insurance policy.

What is Private Supplementary Insurance?

Private health insurance providers offer private supplementary insurance to patients with statutory insurance. With such a policy, you can take advantage of health services that are otherwise reserved for privately insured patients.

Private supplementary insurance is particularly recommended for dental treatment and dentures. Expats in Germany can find high-performance supplementary dental insurance from the digital insurance companies ottonova, Feather, and Getsafe in particular. All three providers have specialized in the requirements of expats with their digital offers and bilingual services.

ottonova and Getsafe also offer supplementary hospital insurance that guarantees statutory health insurance holders treatment by a chief physician and accommodation in single or twin rooms in the hospital.

How Much does Statutory Health Insurance Cost?

The contribution to statutory health insurance funds is currently 14.6% of your gross salary. If you are employed, your employer pays half of this and contributes directly to your health insurance provider.

Freelancers and the self-employed do not receive a subsidy for their health insurance. They can opt for a reduced contribution of 14% if they waive sick pay.

Contributions to statutory long-term care insurance

Long-term care insurance is another compulsory insurance in Germany. The contribution is 3.4% of your gross income; those without children pay 4%. The employer’s contribution is 1.7%.

How to Find the Best Public Health Insurance?

You can choose your health insurance provider in the public health insurance system. Unlike private insurers, statutory health insurance funds must accept all eligible individuals, regardless of age or health status, including serious illness. Waiting periods also do not play a role in public insurance.

Choosing a Good Health Insurance

It would be best to compare several statutory health insurance funds before deciding on a particular health insurance scheme. Important selection criteria are the amount of the additional contributions and the additional benefits of the statutory health insurance funds. On average, many statutory health insurance plans offer similar rates and benefits:

| Medical Expense | Average GKV Price | Coverage Level | Typical Private Insurance Cost | Notes |

|---|---|---|---|---|

| Ambulance | €10 | ~100% | €300–1,000 | Flat copay per use. |

| Advanced Dental Treatment | €500–3,000+ | Partial | €2,000–5,000+ | Supplementary insurance recommended. |

| Basic Dental Treatment | ~20–40% | ~60–80% | €200–2,000+ | Expect a copay under the GKV. |

| Doctor Visit | €0 | 100% | €50–150 | Limited copay under GKV. |

| Emergency Treatment | €0–€10 | ~100% | €500–5,000+ | Limited copay under GKV. |

| Hospital Stay (Per Day) | €10/day (max 28 days/year) | ~99% | €300–1,000/day | Typically capped at €280/year. |

| Preventive Checkups | €0 | 100% | €50–300 | Age-based programs are offered under GKV. |

| Prescription Medication | 10% (min €5, max €10) | ~90–95% | €20–200+ | Price per item can add up over time. |

| Sick Leave Pay (After 6 Weeks) | €0 (income replacement) | ~70% salary | N/A | Standardized in the GKV. |

| Surgery (Non-Cosmetic) | €0 (+ potential hospital fee) | ~100% | €2,000–20,000+ | Includes anesthesia and doctor payment. |

Important: Under statutory health insurance (GKV), most medical costs are covered. Patients pay small, regulated co-payments (“Zuzahlungen”), usually capped and income-linked. For coverage gaps in medical fields like dentistry, it can be advisable to seek supplementary insurance.

Insurance Application, Change of Insurance, Termination

You can apply for insurance with a statutory health insurance company online. You will then get a health card to prove your insurance status at doctor’s visits and with other medical service providers. You can automatically use it in other EU countries as a European Health Insurance Card (EHIC).

A change of statutory health insurance funds is possible after 12 months at the earliest. The standard notice period for cancellation is two months.

A special right of termination applies in the following cases:

- Your annual gross salary rises above the €77,400 (2026) limit.

- You have voluntary statutory health insurance. As your income has fallen, you are now subject to compulsory insurance.

- You are starting as a full-time freelancer or self-employed.

- The conditions for non-contributory insurance are no longer met.

- You have become unemployed.

Conclusion

Statutory health insurance is the basis of the healthcare system in Germany. Contributions depend on income and increase up to the compulsory insurance limit. The benefits provided by statutory health insurance are identical for all insured people. Family members with little or no income can be insured free of charge.

Statutory health insurance companies offer their policyholders various additional benefits. Choosing your provider wisely can optimize your healthcare in the public health system.

Frequently Asked Questions

Yes, the same health insurance regulations apply to expats and German citizens. For a stay of up to one year, you can also take out travel insurance for your health insurance coverage, which non-EU citizens must take out before entering the country. You need statutory or private health insurance if you have lived in Germany for over 12 months.

As an expat, you can take out private insurance if you earn more than €69,300 per year as an employee, are studying in a regular degree program, or work freelance or self-employed.

Freelancers and self-employed people not previously covered by German statutory health insurance, students on language and preparatory courses, and visiting academics without regular employment must take out private insurance.

There is no one-size-fits-all answer to this question. Private health insurance offers a wider range of benefits than public insurance. Young, healthy policyholders usually pay lower premiums. However, you cannot insure your family for free with private insurance.